Article summary: ACA premiums doubled on January 1, 2026, following the expiration of federal subsidies. The average annual cost for marketplace enrollees jumped from $888 to $1,904, a 114% increase. Although the House passed an extension on January 8, the Senate has not moved, leaving 22 million Americans facing a massive “subsidy cliff” and increased healthcare costs.

On December 31, 2025, the federal subsidies that kept Affordable Care Act (ACA) marketplace health insurance affordable for 22 million Americans expired. The House voted to extend them on January 8, 2026. The Senate has not moved. Which means for most people in the coverage gap right now, the subsidies are gone and ACA premiums have gone way up.

What the ACA Premium Numbers Actually Say

The math is simple and ugly. The average subsidized enrollee paid $888 a year for marketplace coverage in 2025. In 2026, that same enrollee is paying $1,904 a year in ACA premiums, a 114% increase, according to KFF, a nonpartisan health policy research organization. For older enrollees in their 50s and 60s, the jump is steeper because insurers are allowed to charge them more than younger buyers for the same plan.Here is what rising ACA premiums in 2026 mean if you are an early retiree under 65 and not yet on Medicare. You are in a coverage window, the years between your last employer plan and the day Medicare starts. For a 57-year-old, that window is 8 years. At the new average ACA premium of $1,904 a month, that window now costs over $182,000 before Medicare begins. That is not a political number. That is a retirement math number.

Your Coverage Window Has a Price Tag Now, and it Punishes You for Earning One Dollar Too Much

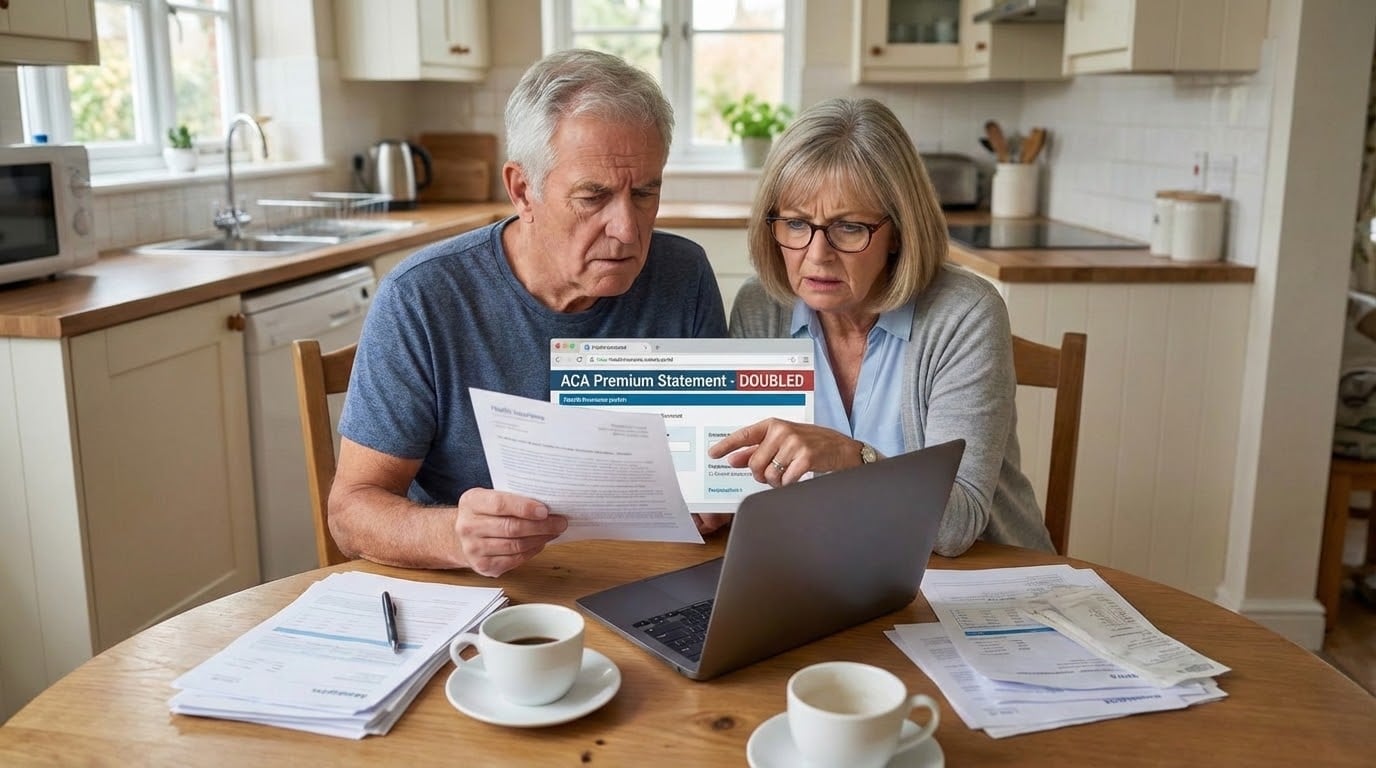

The subsidy cliff makes ACA premiums worse for anyone near the income cutoff. If you are a couple and your combined income is $84,600, you qualify for subsidies. If your income is $84,601, you lose all of them at once. There is no gradual phase-out. A 60-year-old couple earning $85,000 now pays $22,600 more per year in ACA premiums than a couple earning $84,500. One dollar of income. $22,600 in consequences. This cliff existed before 2021, was eliminated during the pandemic years, and came back on January 1, 2026.

Who Controls the Fix and Why It Has Not Moved

Here is who controls the mechanism. The “One Big Beautiful Bill,” passed in summer 2025, did not include a subsidy extension. The House passed a separate three-year extension on January 8, 2026. The Senate has not scheduled a vote. President Trump has signaled he may veto any extension that reaches his desk. In the meantime, 5.5 million Americans between ages 55 and 64 are sitting in the coverage gap with no fix in sight. Worth noting: 88% of ACA enrollment growth since 2020 occurred in states Trump won in 2024. The people most exposed to rising ACA premiums are not the people the mainstream press describes when it covers this story.The real-world toll is already visible. A 64-year-old retiree in Rhode Island is now draining $30,000 from his retirement savings to keep his ACA plan running until Medicare starts. He skipped a colonoscopy this year because the premium ate too much of his budget. A retired couple in Idaho was paying upward of $20,000 a year in healthcare costs before the subsidies expired, and they were bracing for $1,700 a month more in ACA premiums. More than half of Americans who re-enrolled in marketplace plans this year said they are cutting spending on food and clothing to cover the higher costs. One in ten people who had ACA coverage last year are now uninsured altogether. “People like us, we need insurance,” said one retired civil engineer in his early 60s. There is no complicated policy translation needed there.

Three Things to Do Before the Senate Decides Your Retirement Math

If you are in the coverage window right now, there are three things worth knowing. First, check whether your current income puts you near the $84,600 couple threshold. Contributing more to a traditional 401(k) or HSA reduces your taxable income and can pull you back under the cliff, lowering your ACA premiums in the process. Second, ACA marketplace plans are not the only option. Health-sharing ministries operate outside the ACA premium structure and may be worth comparing depending on your health profile and state. Third, if you are within five years of Medicare eligibility, a Medigap or Medicare supplement comparison is worth running now, before the Senate situation changes the market further. If you are in the coverage gap right now and trying to figure out how to manage healthcare costs before Medicare begins, this is the guide most early retirees wish they had before they retired.

If you are in the coverage window right now, there are three things worth knowing. First, check whether your current income puts you near the $84,600 couple threshold. Contributing more to a traditional 401(k) or HSA reduces your taxable income and can pull you back under the cliff, lowering your ACA premiums in the process. Second, ACA marketplace plans are not the only option. Health-sharing ministries operate outside the ACA premium structure and may be worth comparing depending on your health profile and state. Third, if you are within five years of Medicare eligibility, a Medigap or Medicare supplement comparison is worth running now, before the Senate situation changes the market further. If you are in the coverage gap right now and trying to figure out how to manage healthcare costs before Medicare begins, this is the guide most early retirees wish they had before they retired.

The Senate Still Has Time. So Do You.

The House bill is sitting there. Whether it moves before more retirees drain their savings or drop coverage is, at this point, a question of political will. ACA premiums will keep climbing for every month the Senate stalls. You are watching the answer happen in real time.

Frequently Asked Questions:

Why did my ACA premiums go up in 2026?

Your premiums increased because the enhanced federal subsidies from the Inflation Reduction Act expired on December 31, 2025. This caused the average national premium for subsidized marketplace enrollees to rise by 114%, jumping from $888 to $1,904 annually.

What is the ACA “subsidy cliff” for 2026?

The subsidy cliff is a rigid income limit (roughly $84,600 for a couple) where earning one dollar more results in the total loss of federal tax credits. In 2026, crossing this cliff can cost a household an additional $22,600 per year in health insurance premiums.

Has the Senate extended the ACA subsidies yet?

As of April 2026, the Senate has not passed an extension for the ACA subsidies. While the House passed a three-year extension in January, the bill has stalled in the Senate, meaning high ACA premiums will persist until new legislation is signed into law.

Your ACA premiums doubled this year. Who do you think is most responsible? Tell us what you think!