Credit card interest rates are running between 19% and 22% right now, depending on your card, and for anyone carrying a balance month to month, those numbers add up fast. Americans currently hold $1.252 trillion in total credit card debt, according to the Federal Reserve Bank of New York’s Q1 2026 Household Debt and Credit Report. Roughly half of all active cardholders cannot pay their balance in full every month, which means tens of millions of people are watching a significant portion of their payments disappear into interest charges before a dollar touches the principal.

If you are carrying a $5,000 balance at 21% APR, you are paying roughly $87 a month in interest alone. Over a year, that is more than $1,000 that does not go toward your retirement account, your emergency fund, or anything else you planned to do with it.

Why Credit Card Rates Are Still Near Historic Highs in 2026

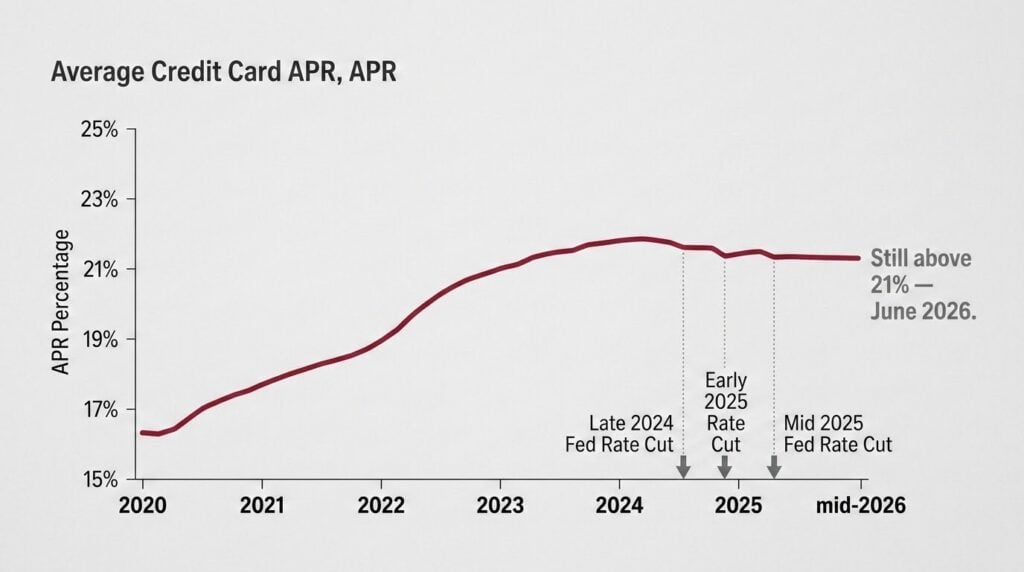

The Federal Reserve cut its benchmark rate three times in 2024 and 2025. Your credit card rate barely moved. That is not an accident.

Your card rate is built on top of something called the Prime Rate, which currently sits at 6.75%. Banks then add their own profit margin on top, and that margin typically runs 12 to 13 percentage points above it. Banks are not required to pass Fed rate cuts through at the same pace, and the data shows they have not.

Despite three Fed rate cuts, the average credit card APR has fallen by less than one percentage point since the cutting cycle began. Bankrate projects rates will fall to roughly 19.1% by the end of 2026 only if the Fed cuts three more times this year. Whether the rate is 21%, 20%, or 19%, the interest bill on a carried balance is still substantial at any of those levels.

What the Federal Reserve’s Rate Cuts Actually Did to Your Card Rate

The Fed’s next scheduled decision is June 18. Markets are currently pricing in a hold, not a cut. That means no relief is coming from that meeting for anyone carrying a balance. The Federal Reserve’s G.19 report shows that the average APR for cards actively accruing interest was 21.52% in Q1 2026. For new card offers, the average is running higher at 23.79%. Experian’s tracking, using Curinos data, puts the broader market average at 19.19% as of May 2026, reflecting a modest pullback from the peak earlier in the cycle.

The range across the market is wide: if you have excellent credit, you may be near the low end, but a standard rewards card almost certainly puts you above 20%. Rates span from 12.20% on the low end to 34.52% at the top, depending on card type, issuer, and credit profile.

The Real Cost of Carrying a Balance at 20%-Plus APR

Here is the math at three common balance levels, using a 21% APR as a baseline.

- $2,500 balance: Approximately $44 per month in interest. About $525 per year going to interest charges before any principal is reduced.

- $5,000 balance: Approximately $87 per month in interest. About $1,050 per year.

- $10,000 balance: Approximately $175 per month in interest. About $2,100 per year.

A $5,000 balance at 21% APR costs over $1,000 in interest annually before a dollar touches the principal. Paying only the minimum on that balance can take over 15 years to eliminate and cost more than $6,000 in interest alone, according to Federal Reserve and CFPB data.

For anyone within 10 years of retirement, every one of those dollar amounts is money that will not be sitting in savings when you get there. Gen X cardholders between 45 and 54 carry the highest average credit card debt of any age group in 2026, at $11,380 per person, with more than half carrying a balance month to month. That cohort is running retirement math and a high-interest debt bill at the same time.

Congress and the White House Proposing to Cap Credit Card Interest Rates

There is institutional movement worth tracking, though none of it has produced relief yet.

President Donald Trump publicly called for a 10% cap on credit card interest rates. Congressional bills currently before the 119th Congress, including S. 381 and H.R. 1944, would cap credit card APRs at 10% through January 2031. Bank of America has been reported to be evaluating whether to offer a card with interest capped at 10% for one year in response to the pressure.

The banking industry is not going quietly. Interest income from credit cards totaled around $120 billion in 2025 among the five largest card-issuing banks alone, comprising roughly a third of their total interest income. That revenue does not disappear without a fight, and the lobbying against a rate cap is well-funded.

Nothing is law yet. The mechanism is documented, the legislation has been introduced, and the political pressure is real. But cardholders waiting on a congressional fix before addressing a carried balance are betting on a timeline nobody can confirm.

How Pre-Retirees Are Responding to Persistent High-Rate Debt

The instinct many people in this situation have had is to take a harder look at what their money is actually doing while they carry high-interest debt.

Savings accounts and money market rates have improved over the past two years, but they are not keeping pace with 20-plus percent card interest. Some people in similar situations have moved a portion of their holdings into assets that aren’t tied to interest rate decisions at all, including precious metals, which tend to hold value independently of what the Fed does with its benchmark rate.

If that is a conversation you have been putting off, Goldco and Birch Gold are two companies that work specifically with pre-retirees looking to diversify away from dollar-denominated savings products. Neither replaces a debt payoff plan, but if your monthly interest statement has been telling you the same thing for the past two years, it may be worth understanding your options.

Researched and fact-checked by the BreakingNewsAlerts.com editorial team. Primary documents verified. Anonymous-source-only claims flagged. See our editorial standards.

Frequently Asked Questions

Why haven’t credit card rates dropped after the Fed’s rate cuts?

Because card rates are built on the Prime Rate plus a bank margin of 12 to 13 percentage points. Banks are not required to pass rate cuts through at the same pace, and the data shows they have not. Average rates dropped less than one point despite three cuts since 2024.

What is the average credit card interest rate right now?

As of Q1 2026, the Federal Reserve’s G.19 report shows the average APR for cards actively accruing interest at 21.52%. New card offers are averaging 23.79%. Experian’s tracking puts the broader market average at 19.19% as of May 2026.

Is a 10% credit card rate cap actually going to happen?

It has been proposed but is not law. S. 381 and H.R. 1944 in the 119th Congress would cap rates at 10% through January 2031. President Trump has publicly backed the idea, but the banking industry is actively lobbying against it. No vote has been scheduled.