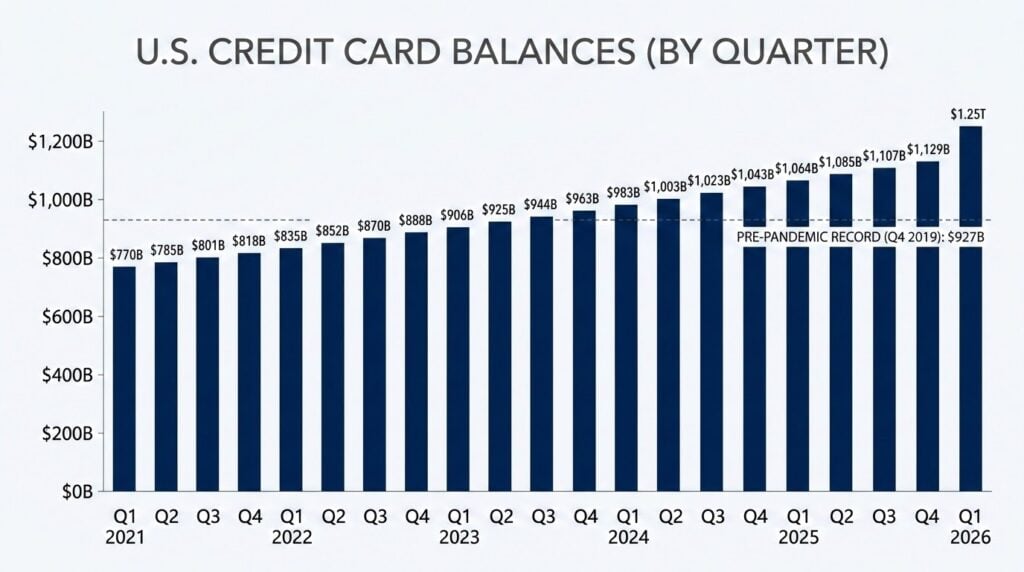

Americans owe $1.25 trillion on their credit cards as of the first quarter of 2026, according to the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit, released May 12. That is $70 billion more than a year ago, a 5.9% annual increase and the highest sustained level of credit card debt since the New York Fed began tracking this data in 1999. Balances dipped $25 billion from Q4 2025’s all-time high of $1.277 trillion, but that decline follows a seasonal pattern that repeats every year after the holidays. The underlying trend has not reversed.

More than half of those balances of 53%, according to a May 2026 Achieve survey of 2,000 consumers, exist to cover essential expenses: groceries, utilities, rent, and healthcare. “For many households, higher balances are less a sign of economic optimism and more a sign that wages and savings are struggling to keep pace with essential expenses like groceries, utilities, and housing,” said Daniel Mangrum, Research Economist at the New York Fed.

That is not the story coming from the White House. National Economic Council Director Kevin Hassett described rising card spending as a sign that consumers have more money in their pockets. The New York Fed’s own data does not support that framing.

How Much Credit Card Debt Are Americans Carrying in 2026?

The scale of the number is one thing. What it costs each month is another. The Federal Reserve’s G.19 consumer credit report puts the average interest rate on accounts carrying a balance at 21.52% as of Q1 2026. The average unpaid balance among cardholders with revolving debt stands at $7,886, according to LendingTree’s analysis of credit report data from Q3 2025.

At 21.52% on a $7,886 balance, a cardholder pays approximately $141 per month in interest or $1,692 per year before a single dollar of principal moves. That is money that cannot go into a retirement account. It cannot go into savings. It compounds in the wrong direction every month the balance stays on the card.

The average American carrying a credit card balance is paying more than $1,600 a year just in interest. That’s money that cannot go toward retirement savings.

Credit card balances have risen 63% since Q1 2021, when the pandemic brought them down to $770 billion. They now sit $325 billion above the pre-pandemic record set in Q4 2019. That five-year climb happened against a backdrop of rate hikes, sustained inflation, and now Fed rate cuts that have not meaningfully moved the needle for cardholders.

What Are Americans Actually Charging to Their Credit Cards?

The composition of what is going on those cards matters as much as the total. The Achieve survey found that 53% of consumers carrying balances are doing so to cover necessities, a finding that aligns with broader research from Empower showing Americans increasingly rely on credit to bridge the gap between wages and the cost of essentials.

Among the Achieve respondents, 57% said it would take six months or longer to pay off their full balance. That timeline carries a compounding cost. A household carrying $7,886 at 25% interest, making minimum payments, will spend 54 months paying it down and fork over $6,384 in interest charges, according to an analysis based on Federal Reserve rate data. That $6,384, invested instead at a 7% annual return over 20 years, would grow to more than $24,700.

Every dollar paid in credit card interest over the next five years is a dollar that will not compound inside a retirement account.

The generational exposure is sharpest for households closest to retirement. Among baby boomers carrying any debt, credit card debt is the most common type — held by 29% of that generation, according to GOBankingRates analysis of 2026 data. Gen X carries the highest average card balance at $7,155. Three in five workers say debt is already hurting their ability to save for retirement, according to Empower research. Twenty-seven percent have reduced or paused retirement contributions entirely because of it.

Why Are Credit Card Interest Rates Still Near 21% Even After Fed Rate Cuts?

The Federal Reserve cut interest rates in 2025. Credit card rates did not follow at the same pace. The average APR on new card offers stands at 23.79% as of Q1 2026, according to LendingTree. For all accounts it’s 21.00%. For accounts actively carrying a balance, it’s 21.52%. A January 2026 Bankrate forecast projected the 2026 year-end average at 19.1%, a decline of less than a full percentage point from where rates started the year.

The reason rates remain elevated while the Fed’s benchmark has fallen comes down to bank profit margins. Analysis published in March 2026 by The Century Foundation and Protect Borrowers found that credit card banks more than doubled their profit margins between 2007 and 2025, a 109% increase in the spread between what banks pay to borrow and what they charge cardholders to carry a balance. Since 2010, Americans have paid a cumulative $2.1 trillion in credit card interest.

The Federal Reserve cut rates. Banks widened their margins. Cardholders absorbed the difference.

The New York Fed’s Q1 2026 data shows aggregate credit card limits continued to rise to $60 billion in the quarter, which means banks are extending more credit even as balances remain near historic highs. The serious delinquency rate on credit cards ticked up year-over-year, from 7.04% in Q1 2025 to 7.10% in Q1 2026, a signal that a growing share of borrowers are already falling behind. The Fed’s rate path and rising borrowing costs have been running in opposite directions for cardholders since 2022.

How Does Credit Card Debt Directly Hurt Retirement Savings?

J.P. Morgan Asset Management’s Retirement by the Numbers research found a direct link between high credit card debt and lower retirement plan balances. Carrying revolving credit card debt reduces the amount workers contribute to defined contribution plans and increases the likelihood of taking early loans against those plans. “Financial health matters, and the financial pressures outside of retirement plans directly affect savings behavior and long-term financial security,” said Michael Conrath, chief retirement strategist at J.P. Morgan Asset Management.

An AARP survey found that 78% of Americans worry Social Security payments will not cover living expenses in retirement, a concern the COLA outlook has done little to ease in recent years. That concern is compounded for households that are simultaneously paying 21% interest on essentials. Every month a balance carries is a month the retirement timeline tightens.

Empower research found that roughly 3 in 5 workers and 3 in 10 retirees say credit card debt is hurting their ability to save for or live comfortably in retirement. For households in the final decade before retirement, the compounding math on a $7,886 balance at 21% does not leave room for error. The pressure on household budgets from debt service compounds the same way student loan restarts have — another drain pulling in the same direction as loan payment obligations.

What Does the $1.25 Trillion Balance Mean for Pre-Retirees?

The five-year trajectory is the clearest signal. Balances rose from $770 billion in Q1 2021 to $1.277 trillion at their Q4 2025 peak — a 66% increase in four years driven not by consumer confidence but by the structural gap between wages and the cost of necessities. For households within a decade of retirement, that gap has a specific cost: it is the money that should be compounding toward a retirement date but is instead compounding toward a bank’s quarterly earnings report.

A pre-retiree carrying an average credit card balance will pay more in interest over the next five years than most Americans contribute to retirement savings in a year.

The inflationary system that pushed essentials onto credit cards in the first place has not reversed. Groceries, utilities, and housing costs remain elevated. Interest rates on new offers are still approaching 24%. The seasonal dip in Q1 2026 is not a structural correction — it is the annual pattern of post-holiday paydown that has repeated every year since tracking began.

Frequently Asked Questions:

Is $1.25 trillion in credit card debt a record high?

It is the highest sustained level since the Federal Reserve Bank of New York began tracking household credit card debt in 1999. The all-time single-quarter peak was $1.277 trillion in Q4 2025. The Q1 2026 figure of $1.25 trillion reflects a typical post-holiday seasonal dip, not a structural reversal.

What is the average credit card debt in the US in 2026?

Americans owe $1.25 trillion in total credit card debt as of Q1 2026, according to the Federal Reserve Bank of New York. Among cardholders carrying an unpaid balance, the average balance is $7,886.

How does credit card debt affect retirement savings?

Carrying credit card debt at an average interest rate of 21.52% means money that could compound in a retirement account is instead paying interest charges. J.P. Morgan Asset Management research found that high credit card debt directly lowers retirement plan balances and increases the likelihood of taking early withdrawals.

Why is credit card debt still high even though interest rates went down?

The Federal Reserve cut its benchmark rate in 2025, but credit card rates followed only marginally. Banks increased their profit margins by 109% between 2007 and 2025 by widening the spread between their cost of borrowing and the rates charged to cardholders. The average APR on accounts carrying a balance is still 21.52% as of Q1 2026.

What percentage of Americans carry credit card debt for essentials?

More than half, or 53%, of consumers carrying credit card balances are doing so to cover essential expenses including groceries, utilities, rent, and healthcare, according to a May 2026 Achieve survey of 2,000 consumers.

How long does it take to pay off the average credit card balance?

At a 25% interest rate, paying off an average balance of $7,886 with minimum payments takes approximately 54 months and costs $6,384 in interest charges alone, according to analysis based on Federal Reserve rate data.