The Parent PLUS loan interest rate is 9.07% for the 2026-27 school year, the highest fixed rate on federal parent loans in more than a decade. It’s been in effect since July 1 for any loan disbursed since, and it will apply to any loan a parent cosigns for the fall semester. Add the loan’s origination fee, deducted before a single dollar reaches the tuition bill, and the real first-year cost tops 13%. For parents close to retirement who are cosigning for a child headed to college, that number changes how much they can safely commit.

The rate is not random. Congress set the formula years ago: take the yield from the 10-year Treasury Note auction each May, then add a fixed margin by loan type. This year’s auction produced a yield of 4.468%. For Parent PLUS loans, the margin is 4.60 points.

What Is the Parent PLUS Loan Interest Rate for 2026-27?

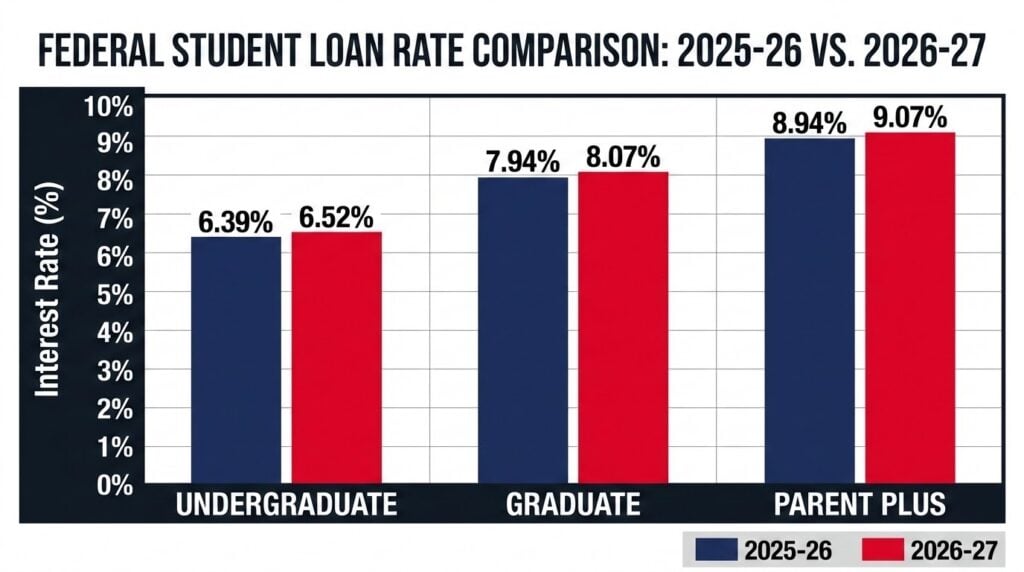

Every federal loan rate ticked up this year, not just Parent PLUS. Undergraduate loans rose from 6.39% to 6.52%. Graduate loans rose from 7.94% to 8.07%. The Parent PLUS rate is 9.07% for loans disbursed July 1, 2026 through June 30, 2027, still the highest of the three. PLUS loans also carry a cost undergraduate and graduate loans don’t: that 4.228% origination fee, taken off the top before the school ever sees the money.

What Will a New Parent PLUS Loan Cost You This Fall?

Parents cosigning a Parent PLUS loan for the first time this year face one piece of good news buried in the bad. Under the law President Donald Trump signed last year, the formerly unlimited Parent PLUS borrowing is now capped at $20,000 a year and $65,000 total per child. Families can no longer borrow the full cost of attendance. This limits how deep a parent can go into debt for a single school year, even if it means covering the rest of the bill another way.

The tradeoff: loans taken out after July 1, 2026 lose access to income-driven repayment. The standard repayment plan is now the only option, a fixed monthly bill regardless of income, right as many cosigning parents are approaching their own retirement income.

What’s the September 30 Deadline for Existing Parent PLUS Borrowers?

Parents who already have a Parent PLUS loan in repayment have a real, near-term move available. Payment rules already changed once this year, when the pause ended and wage garnishment resumed. Now there’s a new lever: the Department of Education announced on June 18 that borrowers enrolled in autopay by September 30, 2026 get a full percentage point knocked off their interest rate, up from the previous quarter-point discount. The reduction runs through June 30, 2028, and applies to any Direct Loan, including Parent PLUS, first disbursed on or after July 1, 2012 and currently in repayment.

What Happens If You Default on a Parent PLUS Loan?

Parent PLUS loans carry consequences beyond a higher bill if payments lapse. Default can trigger wage garnishment and, for parents already collecting Social Security, garnishment of monthly benefit checks. There is no bankruptcy shortcut, and no way to shift the loan into a child’s name without refinancing through a private lender, which forfeits federal protections for loans disbursed before July 2026.

Either way, the math comes down to the same question: how much of your own retirement runway are you willing to spend on a loan that legally can’t be transferred to your child’s name? That’s worth working out before signing anything this fall, or before your next autopay cycle locks in.

For parents managing a Parent PLUS balance while trying to protect what they’ve saved for retirement, the numbers above are the starting point, not the whole plan. The Total Money Makeover by Dave Ramsey lays out a step-by-step framework for paying down debt without sacrificing the retirement savings still ahead of you.

![The Total Money Makeover Set : The Total Money Makeover [hardcover] & The Total Money Makeover Workbook [paperback]](https://m.media-amazon.com/images/I/41oAYsglTtL._SL160_.jpg)

BreakingNewsAlerts.com may earn a commission on purchases made through this link, at no extra cost to you.

Frequently Asked Questions

What is the Parent PLUS loan interest rate for 2026-27?

This year’s interest rate is 9.07%, which is up from 8.94% for 2025-26, plus a 4.228% origination fee deducted before disbursement.

How much can I borrow with a Parent PLUS loan now?

New borrowers are capped at $20,000 a year and $65,000 total per child starting July 1, 2026, replacing the previous unlimited borrowing rule.

Can I lower my Parent PLUS loan interest rate?

Yes if your loan was already disbursed after July 1, 2012, and you’re in repayment. Enrolling in autopay by September 30, 2026 cuts the rate by a full point through June 2028.

What happens if I default on a Parent PLUS loan?

The Department of Education can garnish wages and, for parents collecting Social Security, garnish monthly benefit checks. There is no way to transfer the loan to your child’s name without a private refinance.