The Senior Citizens League raised its 2027 Social Security COLA forecast to 3.9% on May 12. That is up from 3.2% in April, 2.8% in February, and 1.2% in January. Four upward revisions in four months. Each one means inflation moved faster than the prior month’s math predicted. Is the 2027 Social Security COLA not enough?

The number is not rising because things are getting better. It is rising because the damage is getting worse.

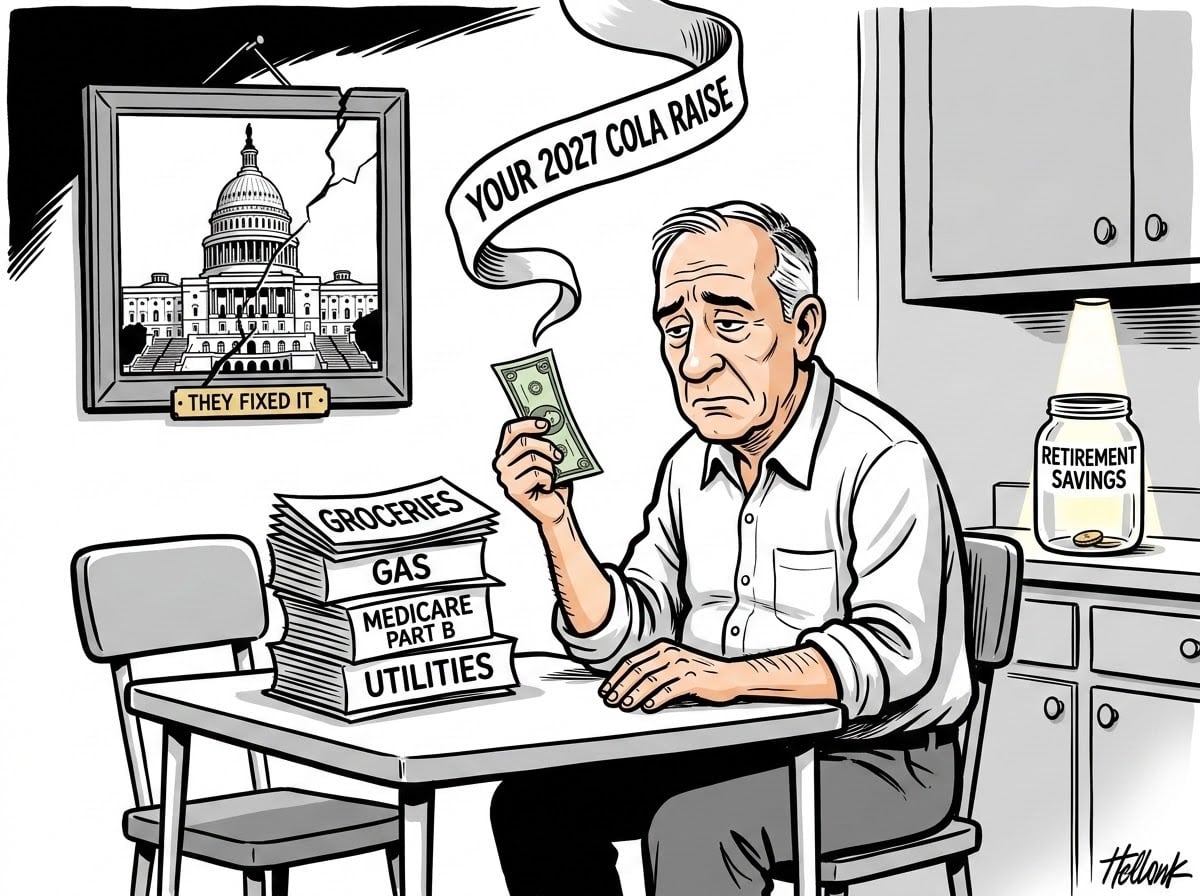

The average retired worker currently receives $2,081.16 per month. At 3.9%, the gross projected increase is about $81 per month, or $972 for the full year. Before Medicare takes its cut.

The standard Medicare Part B premium rose 9.7% in 2026 to $202.90 per month, up from $185 the year before. The 2026 COLA added roughly $57 to the average check. The Part B increase took $17.90 of it back. Net gain for the average retiree: about $38 per month.

The 2027 Part B premium will not be announced until November. If the three-year pattern holds, expect it to consume one-third or more of whatever the gross COLA lands at. For most retirees, the real net monthly increase will be closer to $54. For anyone in an IRMAA income tier, it gets worse from there.

Why Does the 2027 COLA Forecast Keep Rising Every Month?

The Consumer Price Index for Urban Wage Earners and Clerical Workers, the CPI-W, hit 3.8% in April, up from 3.3% in March. That 0.5-point jump in a single month is not typical. The Federal Reserve Bank of Cleveland’s inflation forecasting tool showed CPI trending above 4% in May.

The 3.9% projection is based on April data that is already a month old. The official 2027 COLA will not be calculated until the Social Security Administration compares third-quarter CPI-W readings from July, August, and September against the same months in 2025. The announcement comes in mid-October. The first increased check arrives in January 2027.

Retirees absorb higher gas, grocery, and utility prices now. The adjustment arrives eight to ten months later. Independent Social Security analyst Michael Ryan described the timing to Newsweek as “an insurance check after the house already caught fire.”

The COLA forecast has risen every month since January because inflation has accelerated every month since January, and the check that compensates for that acceleration does not arrive until January 2027.

Why Doesn’t the Social Security COLA Formula Measure What Retirees Actually Spend?

The CPI-W measures the spending patterns of urban wage earners and clerical workers. That group represents about 30% of the U.S. population. Retirees are not in it.

Households led by someone 75 or older spend roughly 16% of their budget on medical care. Younger working households spend closer to 3.8%. Medical prices rose 3.4% in the 12 months through February 2026. The CPI-W registered 2.2% over the same window. The formula undercounts the costs retirees actually face because it was never designed to count them.

The Senior Citizens League calculates that Social Security purchasing power has dropped 20% since 2010. Even the record 8.7% COLA in 2023 fell short. Inflation that year ran at 7% broadly, but retirees’ healthcare and housing costs ran higher.

Readers commenting on a Medicare Rights Center post put it plainly. “CPI has never been a true cost of living as far as COLA,” one wrote. “Give one place, take it away elsewhere. It’s never an increase. Premium goes up. All said and done, farther behind.”

The CPI-W formula excludes retirees entirely and undercounts healthcare costs that consume roughly 16% of a senior household’s budget — the reason Social Security purchasing power has fallen 20% since 2010, even in years with above-average COLAs.

What Will the 2027 COLA Actually Mean for Your Monthly Deposit After Medicare?

The gross number and the deposit number are not the same figure. Here is what the math looks like before the November Part B announcement.

Average retired worker benefit: $2,081.16. At 3.9%, gross monthly increase: approximately $81. Medicare Part B consumed $17.90 of the average 2026 COLA increase. If the same pattern holds in 2027, roughly $27 of the $81 goes back to the Centers for Medicare and Medicaid Services before it reaches the bank account. Net monthly gain for the average retiree: approximately $54.

For retirees in the first IRMAA income tier, the math is harder. Single filers with modified adjusted gross income above $109,000 and couples above $218,000 pay Part B at $284.10 per month rather than $202.90. That is an $81.20 monthly difference triggered by one dollar of income over the threshold. A Roth conversion, a home sale, or a required minimum distribution taken at 73 can all push a retiree across that line using income from two tax years prior.

The hold harmless provision prevents Medicare Part B premiums from wiping out a COLA entirely for most beneficiaries. But new enrollees and higher-income retirees are excluded from that protection entirely.

For the average retiree, the 2027 COLA gross increase of roughly $81 per month becomes approximately $54 after Medicare Part B takes its share — and for retirees in IRMAA tiers, the Medicare offset can consume 50% to 72% of the gross increase.

Social Security COLA Not Enough: But How Does a Higher COLA Make the Problem Worse?

A higher COLA does not just fail to help retirees keep pace. It actively accelerates the trust fund insolvency timeline.

The Committee for a Responsible Federal Budget stated that if the projected COLA materializes without a matching increase in wage growth, it would worsen Social Security’s shortfall by roughly $300 billion over the next decade and advance the insolvency of the old-age trust fund by three months, from late 2032 to earlier in the year. The Social Security old-age trust fund is already projected by the Congressional Budget Office to face depletion by 2032, at which point the law requires automatic benefit cuts of approximately 25% to 28%.

COLA increases are permanent. Once a raise takes effect, it becomes the new baseline. Every future adjustment compounds on top of it. Across more than 70 million beneficiaries, a single percentage point difference adds up to hundreds of billions over a decade. A bigger COLA today, driven by inflation that exceeds wage growth, borrows against the benefit Raymond is counting on in 2032.

A 3.9% COLA driven by inflation without matching wage growth adds an estimated $300 billion to Social Security’s long-term shortfall and pulls the trust fund’s depletion date three months closer — meaning a bigger raise today makes the eventual automatic benefit cut more likely to arrive on schedule.

What Steps Can Retirees Take Before the Official October COLA Announcement?

The 2027 COLA will be whatever the July, August, and September CPI-W data produce. That number is not in anyone’s hands right now. What is in your hands:

Medicare open enrollment runs from October 15 through December 7. Reviewing Part D and Medicare Advantage plans on Medicare’s Plan Finder at Medicare.gov before that window opens costs nothing. Retirees who stay on the same plan year after year routinely leave hundreds of dollars on the table. The official COLA announcement lands on October 14 — one day before the enrollment window opens. Review both at the same time.

Know your IRMAA thresholds before the October announcement. Single filers at $109,000 modified adjusted gross income. Couples at $218,000. Review the 2024 tax return now. A large Roth conversion, a home sale with gains above the $500,000 couples exclusion, or a required minimum distribution at 73 can all trigger a threshold crossing that raises Part B from $202.90 to $284.10 per month, based on income reported two years prior.

Pressure-test your net number. Whatever the gross COLA is announced at in October, subtract a projected Part B increase before building any budget around it. Based on the prior three years, the Part B increase has consumed between one-third and 9.7% of the headline COLA in gross dollar terms. The headline figure and the deposit figure will not be the same number.

Retirees have three concrete actions before October: review Medicare plan options before the enrollment window opens on October 15, audit 2024 income for IRMAA threshold exposure, and pressure-test the net COLA deposit rather than budgeting around the gross announcement figure.

Frequently Asked Questions

When will the official 2027 Social Security COLA be announced?

The Social Security Administration will announce the official 2027 COLA on October 14, 2026, after the Bureau of Labor Statistics publishes July, August, and September CPI-W readings. The first adjusted payment arrives in January 2027.

How much of the 2027 COLA will Medicare Part B consume?

Based on 2026 data, the standard Medicare Part B premium rose $17.90 to $202.90, consuming roughly one-third of the average COLA increase. The 2027 premium will be announced by CMS in November 2026. Retirees in IRMAA income tiers above $109,000 single or $218,000 joint face steeper offsets, ranging from 50% to 72% of the gross COLA increase.

Why does the Social Security COLA keep falling short of actual retiree costs?

The COLA formula tracks the CPI-W, which measures spending patterns for urban wage earners, not retirees. Retirees allocate roughly 16% of their budget to healthcare versus about 3.8% for working-age households. Medical prices consistently rise faster than the CPI-W captures, causing cumulative purchasing power erosion the Senior Citizens League estimates at 20% since 2010.

Can a higher COLA actually hurt Social Security’s long-term finances?

Yes. A COLA driven by inflation exceeding wage growth increases benefit outlays without a corresponding revenue increase. The Committee for a Responsible Federal Budget estimates this dynamic would worsen the program’s long-term shortfall by $300 billion over a decade and pull the old-age trust fund’s depletion date forward from late 2032 to earlier in the year.

What is the IRMAA threshold retirees need to watch before the 2027 COLA takes effect?

Single filers with modified adjusted gross income above $109,000 and couples above $218,000 move into the first IRMAA tier, raising the standard Part B premium from $202.90 to $284.10 per month. Events that can trigger a threshold crossing include Roth conversions, home sales, and required minimum distributions taken at age 73, all calculated using income from two tax years prior.