QUICK SUMMARY: The Iran war pushed U.S. gasoline prices up 21.2% in March, the steepest monthly jump since 1967. Analyst Mary Johnson nearly tripled her 2027 Social Security COLA forecast in response, from 1.2% to 3.2%. But retirees pay higher prices now. The COLA does not arrive until January 2027, and Medicare Part B will take a cut.

The 2027 Social Security COLA forecast just jumped because of the Iran war. Independent analyst Mary Johnson raised her projection to 3.2% in April from 1.2% in February, a near-tripling driven by the energy supply shock. Meanwhile, the Senior Citizens League projects 2.8%. Some financial outlets, including Motley Fool and Yahoo Finance, are framing the jump as a raise. That framing is misleading.

A higher 2027 Social Security COLA is not a raise. It is a late, partial, formula-flawed reimbursement for losses retirees have already absorbed at the pump and the grocery store. Medicare Part B will consume a cut of whatever arrives.

Retirees already know this in their bones. A commenter on a Motley Fool retirement column put it plainly in March: “Horse pucky! I laugh when I read the government’s cost of living data, and cry when I see my COLA.”

How the Iran War Reached Your Social Security Check

The mechanism explains why the relief arrives late.

The Bureau of Labor Statistics tracks monthly price changes through the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as CPI-W. The Social Security Administration takes the July, August, and September 2026 CPI-W averages, compares them to the same months in 2025, and sets the 2027 COLA based on the difference. The announcement comes in mid-October. The first increased check lands in January 2027.

Energy costs make up 6.2% of the CPI-W formula. When Iran war damage to Gulf Arab oil facilities tightened global oil supply, U.S. gasoline prices surged 21.2% in March. That was the largest single-month gas price jump since 1967. Annual inflation climbed to 3.3%, up from 2.4% in February, the biggest monthly inflation increase in nearly four years.

The 2027 COLA forecast moved on that data. As reported by Fox Business, the Senior Citizens League now estimates 2.8% for 2027. Mary Johnson’s separate forecast jumped higher.

Kathryn Price Engelhard, a 70-year-old retired nonprofit director in Pennsylvania, told PBS NewsHour in March what any retiree with a calendar could have predicted. “I look at the prices of oil in the past and the stupid war, how did we, how did anybody, think that that was not going to impact oil?”

The Raise Arrives After the Damage Is Done

The COLA is structurally backward-looking. It measures inflation that has already happened.

A Social Security beneficiary absorbs higher gas, grocery, and utility prices in March, April, May, and June. The 2027 COLA is not announced until mid-October 2026. The first increased check does not arrive until January 2027.

Finance expert Michael Ryan described it to Newsweek in March as “an insurance check after the house already caught fire.” The math backs him up. Beneficiaries feel higher gas and grocery bills immediately. Social Security does not catch up for nearly a year.

The Medicare Cut Nobody Mentions

The second piece of the story some financial outlets are skipping is Medicare Part B.

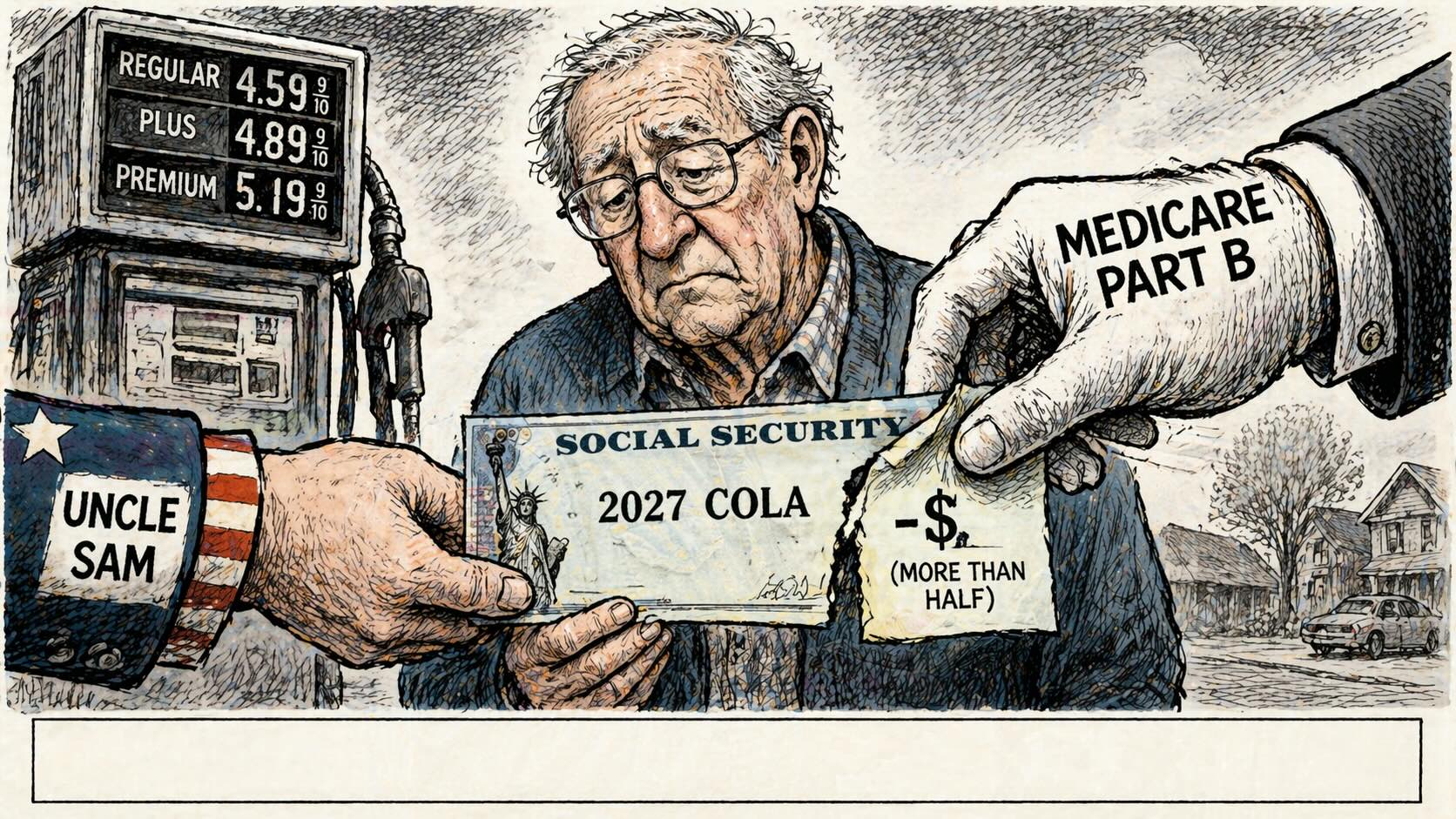

The standard Medicare Part B premium rose to $202.90 per month in 2026. That is up $17.90 from $185 in 2025, a 9.7% premium increase. It is roughly three times the size of the 2026 COLA. The premium is deducted automatically from the Social Security check before the money reaches the bank account.

The math on the average benefit is stark. A 2.8% COLA added about $57 per month to the average retired worker’s check. The Part B increase ate $17.90 of it. Net gain: about $38 per month.

For retirees in IRMAA income tiers, the damage is worse. In 2026, retirees in the first IRMAA tier saw Part B consume 50% of their COLA increase. Second-tier retirees lost 72%. Cross the $109,000 single-filer MAGI threshold by a single dollar and the 2026 Part B premium jumps from $202.90 to $284.10 per month, a $974 annual hit triggered by tax return income from two years prior.

The 2027 Part B premium will be announced by the Centers for Medicare and Medicaid Services in November 2026. If the pattern holds, expect the Part B increase to take one-third or more of whatever 2027 Social Security COLA is announced.

The Formula Was Built Against Retirees

The CPI-W measures the spending patterns of urban wage earners and clerical workers. That group represents about 30% of the population. Retirees are not in it.

Households led by someone 75 or older spend about 16% of their budget on medical care. Younger households spend closer to 3.8%. Medical prices rose 3.4% in the 12 months through February 2026. The CPI-W increased just 2.2% over the same window.

The Senior Citizens League calculates that Social Security purchasing power has dropped 20% from 2010 to 2024. A Motley Fool survey this winter found that 54% of retirees called the 2.8% COLA insufficient. 68% said the boost would do little to help cover essential living expenses.

Aaron Brachman at Steward Partners put it to U.S. News, in blunt terms: The COLA formula is “laughably misaligned with the expenses seniors have.”

What You Can Actually Do Before January

The 2027 number is not locked. But what you do between now and January is in your hands.

- Watch Medicare open enrollment. The window runs from October 15 through December 7, 2026. Review Part D and Medicare Advantage plans on Medicare’s Plan Finder at Medicare.gov. Retirees who stay on the same plan year after year routinely leave hundreds of dollars on the table.

- Know the IRMAA thresholds. Single filer $109,000 MAGI. Couples $218,000 MAGI. One dollar over the line can push Part B from $202.90 to $284.10 per month. A large Roth conversion, a home sale with gains above the $500,000 couples exclusion, or a required minimum distribution at 73 can all trigger it.

- Pressure-test your budget. Whatever the 2027 Social Security COLA lands at, subtract the expected Part B premium increase before planning around it. Assume the real net increase is about two-thirds of the headline number.

The story this spring is not that retirees are getting a raise. The story is that retirees already paid for it at the pump, at the grocery store, and on the utility bill. The money arrives late, reduced, and for many, taxed. That is not a raise. That is a receipt.

The COLA formula is not changing between now and January. The Medicare Part B premium calculation is not changing either. What you can change is how prepared you are when those numbers land. A clear, updated reference on how Social Security actually works, including COLA mechanics, Medicare integration, and the IRMAA tiers that catch retirees off guard, is worth more before the October announcement than after it.

Frequently Asked Questions

When will the 2027 Social Security COLA be announced?

The Social Security Administration announces the official figure in mid-October 2026, after the Bureau of Labor Statistics publishes September CPI-W data. The increase takes effect in January 2027.

Why doesn’t my COLA match the inflation I actually feel?

The COLA formula uses CPI-W, which tracks spending patterns for urban working-age wage earners. Retirees spend far more on healthcare and housing, both of which rise faster than the basket the formula measures. The Senior Citizens League calculates that Social Security buying power has dropped 20% since 2010.

Will the Iran war keep gas prices high through the summer?

The 2027 COLA is calculated from CPI-W readings in July, August, and September 2026. If gas prices stay elevated through those months, the COLA rises. If the war ends and oil prices fall significantly by summer, the forecast drops back toward earlier estimates. The answer is in the hands of the Iranian leadership and the Gulf oil infrastructure, not U.S. policy.

How much of my 2027 raise will Medicare actually take?

In 2026, the standard Medicare Part B premium rose $17.90 to $202.90, roughly 36% of the average COLA increase. The 2027 Part B premium will be announced by CMS in November 2026. If the pattern holds, expect the Part B increase to consume one-third or more of whatever COLA is announced. For retirees in IRMAA tiers, the consumption rate can reach 50% to 72%.