The U.S. economy added 57,000 jobs in June, the Bureau of Labor Statistics reported July 2, roughly half the 115,000 economists had forecast. The unemployment rate dropped to 4.2%. Most coverage stopped there and called it good news.

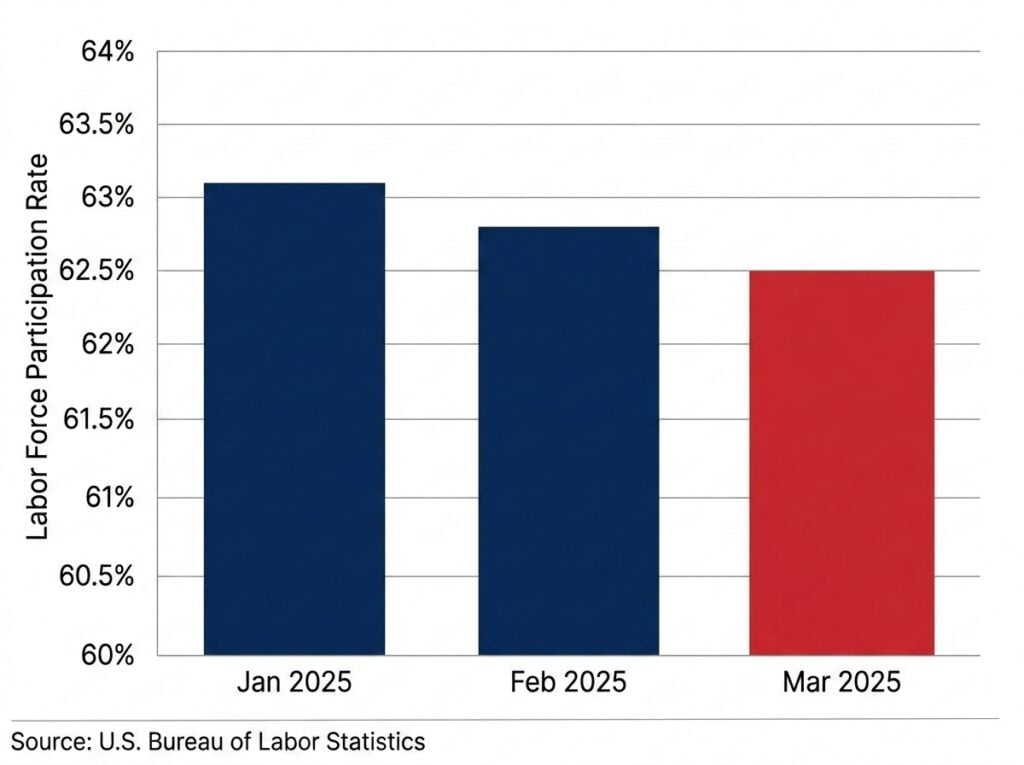

It isn’t. The drop happened because 720,000 people left the labor force in a single month, not because more people found work. The number of people actually employed, measured separately in BLS’s household survey, fell by 507,000. The share of working-age adults either employed or actively looking for work, the labor force participation rate, fell to 61.5%, the lowest since March 2021, and outside the pandemic, the lowest since June 1976.

If you’re eight to ten years from claiming Social Security, this is the number that touches you directly. A shrinking labor force means fewer workers paying into the system that funds your benefit. It also means the “healthy” unemployment rate in this week’s headlines is measuring the wrong thing. As our earlier reporting on Social Security’s 2032 funding deadline showed, the trust fund is already running on a tighter timeline than most retirees realize. Fewer workers paying in doesn’t move that date in your favor.

Why Did Real Wages Fall for a Third Straight Month?

The report showed average hourly earnings rose 3.5% over the past year. Inflation is still running above 4%, meaning real wages fell for a third straight month, a raise on paper and a pay cut in practice. Dan North, senior economist for North America at Allianz, called the participation drop “a big leg down” and said the numbers were “cause for concern,” pushing back on the idea that retirements alone explain what happened.

He has a point worth sitting with: the steepest decline wasn’t retirees. It was prime-age workers, 25 to 54, the group least likely to be stepping back voluntarily. Their participation rate fell to 83.3%, the lowest since December 2023.

Households are already absorbing this squeeze from more than one direction. Credit card debt hit $1.25 trillion this quarter. A weaker paycheck landing on top of that is not two separate problems. It’s the same one, from two angles.

What Does the Fed Chair Do Next?

Federal Reserve Chair Kevin Warsh called the labor picture “steady” this week, while keeping his focus on getting inflation back to the Fed’s 2% target. The Federal Open Market Committee’s July 8 minutes, from a meeting held before this weaker print landed, already showed several officials leaning toward a rate hike before year-end. Futures markets are now pricing meaningful odds of a move as early as September, according to the CME FedWatch Tool.

That matters for anyone with savings sitting in CDs, money markets, or fixed income heading into retirement. A rate hike changes what your cash earns and what your next loan costs, at the exact moment your income is about to shift from a paycheck to a fixed monthly benefit. Warsh’s approach to inflation has been on the record since his first meeting in June, and it hasn’t moved in the direction that helps a saver.

As one reader on the financial newsletter Modern Exodus put it, seeing the participation numbers: “How many of those are retirees?” It’s the right question. BLS data says the honest answer is: not as many as this week’s headlines suggest.

What This Means for Your Retirement Timeline

Nothing here demands a decision today. There’s no enrollment deadline, no single date on a calendar. What changed is the information you’re working with. A weakening labor force funding Social Security, wages still losing ground to prices, and a Fed chair with room to raise rates rather than cut them, that’s a different retirement math than the “steady” story most coverage ran this week.

The honest move is to know exactly where you stand before the next report changes the picture again, not to guess.

If you’re within a decade of claiming Social Security, the biggest mistake most retirees make isn’t about the stock market, it’s about when they file. Get What’s Yours: The Secrets to Maxing Out Your Social Security by Laurence Kotlikoff, Philip Moeller, and Paul Solman breaks down filing strategies most people never hear from the Social Security office itself.

Frequently Asked Questions

Did the June jobs report actually show a stronger economy?

No. The headline unemployment rate fell, but BLS data shows that happened because 720,000 people left the labor force, not because hiring picked up. The number of people actually employed fell by 507,000 in June.

What is the labor force participation rate, and why does it matter?

It measures the share of working-age adults who are either employed or actively looking for work. It fell to 61.5% in June, the lowest since March 2021 and, outside the pandemic, the lowest since 1976. A shrinking labor force means fewer workers supporting Social Security and Medicare.

Will the Federal Reserve raise interest rates because of this report?

Uncertain. Fed Chair Kevin Warsh has emphasized bringing inflation to the 2% target, and the FOMC’s July 8 minutes showed several officials open to a hike before year-end. Futures markets are pricing meaningful odds of a move as early as September.

How does labor force participation affect Social Security’s funding?

Fewer workers paying payroll taxes narrows the funding base supporting current benefits, though it doesn’t change your individual benefit formula.

Should retirees change their Social Security filing plans because of this report?

No single jobs report should drive a filing decision. It’s a signal to review your timeline, not a reason to act on this data alone.