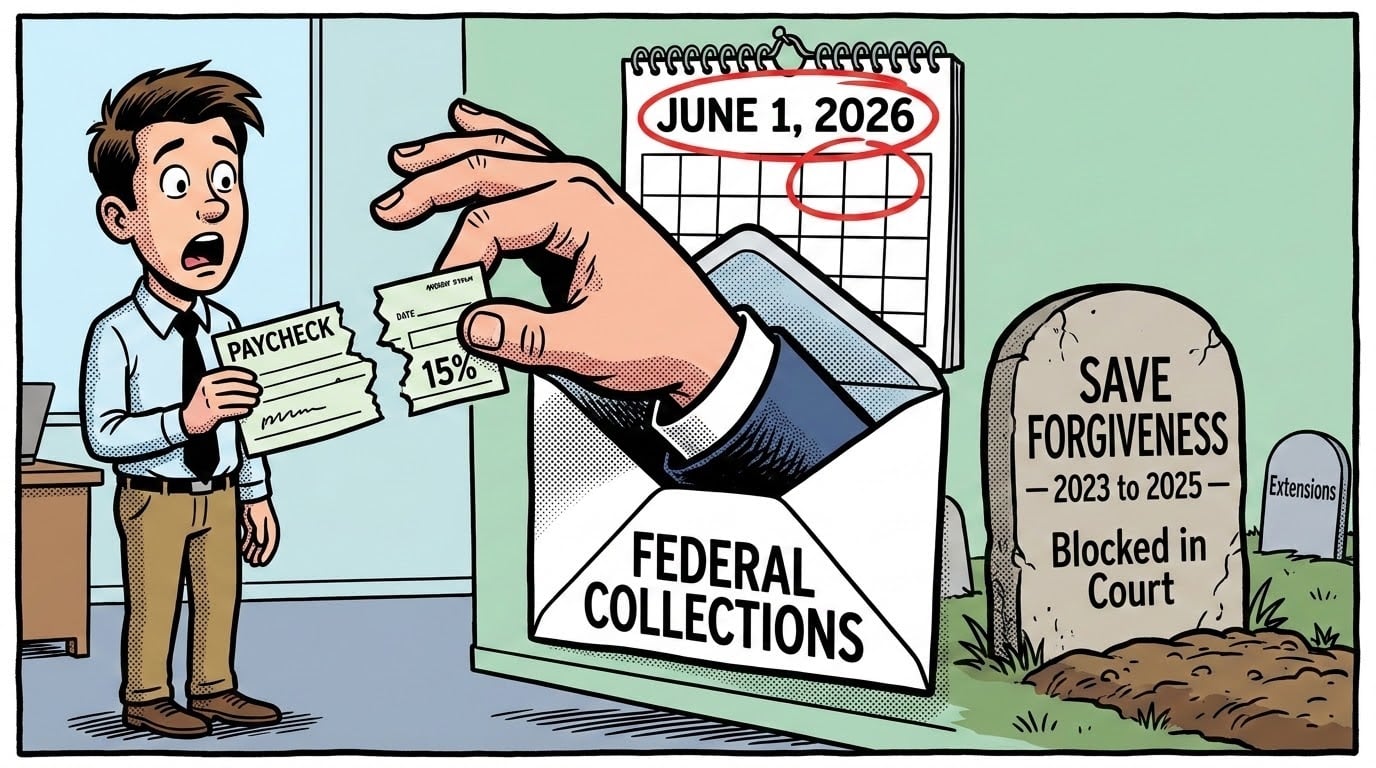

The federal student loan payment pause ends on June 1, 2026. About 28 million borrowers are back on the hook for monthly payments that average $200 to $500. The Department of Education has also restarted wage garnishment for borrowers who are in default, which means the government can take up to 15% of their take-home pay. The first notices went out the week of January 7, 2026.

This is not the same restart that happened back in October 2023. The rules have changed under the One Big Beautiful Bill Act, the SAVE forgiveness program is dead, and Public Service Loan Forgiveness just got harder to qualify for. Anyone who has been waiting for one more pause or extension has run out of time.

Why Are Most Borrowers Not Caught Up After Five Years?

The pause first started in March 2020, during the first Trump administration. President Biden extended it several times after taking office. Payments officially restarted in October 2023, but the government didn’t push hard on collections during that period. The SAVE plan promised lower payments and faster forgiveness, but it ended up tied up in court. Then in 2025, the One Big Beautiful Bill Act overhauled the entire federal student loan system from the top down.

That’s five years of pauses, restarts, and major rule changes across three administrations. It is no wonder a lot of borrowers genuinely feel lost on where they stand right now. A financial industry expert who works with defaulted borrowers recently told CBS News that the harsh penalties tied to student loans have “left the collective consciousness.” That gap between what the rules actually are and what borrowers remember is the real story here.

How Much Will the Restart Cost the Average Household?

The median federal student loan payment is roughly $300 a month. For about one in five borrowers, it climbs above $500. That works out to somewhere between $3,600 and $6,000 a year coming out of a household budget that adjusted to that money being absent for half a decade.

If you are the parent of a borrower, your adult kids almost certainly know their balances and their loan servicers better than you do. They already know their numbers. They have been managing their own accounts for years. What they may not realize is that the rules just changed underneath them while almost everyone was watching the SAVE lawsuit play out. The kids who hear about the policy shift from a parent who reads the news are the kids who do not get blindsided.

If you are reading this through the lens of your own retirement window, the story matters differently. About 28 million borrowers cutting back on everyday spending is a real drag on the broader consumer economy. Bloomberg flagged the same dynamic during the 2023 restart cycle. This time around, the group is larger and the enforcement is tougher. The economy you are planning to retire into is the same economy carrying this restart.

What’s Different About the Student Loan Payment Restart in 2026?

Five things have changed since the last restart in October 2023. Borrowers who tuned out at any point during the SAVE plan court fight are likely missing at least three of them.

- Wage Garnishment Is Back.

The first notices started going out the week of January 7, 2026. The federal government can take up to 15% of take-home pay from any borrower who has been in default for 270 days or longer. About 5.5 million borrowers are already in default, and another 4 million are getting close. Every missed student loan payment now counts toward that 270-day threshold. - The SAVE Forgiveness Pathway Is Dead.

The plan that promised faster forgiveness for low-balance borrowers and lower monthly payments was blocked in court, and the Department is winding it down for good. Education Secretary Linda McMahon was unambiguous in the Department of Education’s April 2025 press release announcing the collections restart: “There will not be any mass loan forgiveness.” Borrowers who were enrolled in SAVE need to pick a new plan, or they will get rolled into the standard repayment plan automatically. - Income-Driven Repayment Is Phasing Out.

The income-driven repayment plans that most borrowers have been using are being replaced under the new law. They are being swapped out for the standard plan and a new program called the Repayment Assistance Plan. Borrowers on the older plans need to confirm which plan they are actually on right now. - PSLF Eligibility Just Got Narrower.

The One Big Beautiful Bill Act tightened the rules for Public Service Loan Forgiveness. Some borrowers who were on track under the previous criteria may not qualify anymore. The changes mostly affect which employers count and which payment counts go toward forgiveness. - Parent PLUS Is Changing on July 1.

New borrowing caps of $20,000 per year and $65,000 per dependent student take effect on July 1, 2026. In-school deferment, which let borrowers pause payments while their student was enrolled, ends for any federal loans taken out after that date.

Is Student Loan Forgiveness Still Possible in 2026?

For certain narrow categories of borrowers, yes. Borrowers in qualifying public service jobs who meet the tightened PSLF rules can still pursue forgiveness. Borrowers with documented borrower defense claims can still file those claims and pursue relief. But for the broader population of federal student loan borrowers, the courts have closed the path the previous administration tried to open. The current rules are what borrowers have to plan around for now.

Disclosure: This article contains affiliate links. If you use them, BreakingNewsAlerts.com may earn a commission at no cost to you. Our editorial picks are independent of these partnerships. See our editorial standards.

If the Payment Math Does Not Work for a Household

The math simply does not work for everyone. Some borrowers are refinancing their higher-interest private loans to free up room in their budget for the federal payment. LendingClub is one of the platforms working in this space. Some borrowers are using a paycheck-timing tool like Earnin to bridge the gap between when the loan payment lands and when payday actually arrives. Neither one is a fix for the underlying policy. They are just tools to help a household keep functioning until something else changes.

For more on how federal benefit changes are hitting retirement-age households, see our coverage of the three Medicare benefit changes affecting retirees this year.

If Your Adult Kids Don’t Read the News, Forward This

Most borrowers know their own loans pretty well. What they may not realize is that the rules changed while they were waiting on an extension that isn’t coming. June 1 is the deadline, and wage garnishment is already running for borrowers in default. The student loan payment landscape isn’t what it was back when the pause started in 2020. This is the kind of update that doesn’t usually trend on social feeds and doesn’t lead the evening news, but it lands in the household either way.

Verify your loan and check the latest plan options at studentaid.gov.

Frequently Asked Questions

Can the government garnish wages for unpaid student loans in 2026?

Yes. The federal government can take up to 15% of take-home pay from borrowers who are 270 days or more in default. The first notices went out the week of January 7, 2026.

Is SAVE forgiveness still available?

No. The plan was blocked in court and is being formally wound down. Enrolled borrowers need to pick a new plan, or they will get rolled into the standard plan automatically.

Does Public Service Loan Forgiveness still exist?

Yes, but eligibility tightened under the One Big Beautiful Bill Act. Some borrowers who were on track under the previous rules may no longer qualify.

What changes for Parent PLUS loans on July 1, 2026?

New borrowing caps of $20,000 per year and $65,000 per dependent student take effect. In-school deferment also ends for new federal loans taken out after that date.

What is the average federal student loan payment in 2026?

The median is about $300 a month. Roughly one in five borrowers pays $500 or more, based on prior-cycle TransUnion analysis.